In less than a generation, the media industry has undergone a series of innovations that have totally revolutionized the relationship between consumers and content producers. This revolution, which has taken place at the expense of traditional media such as press, radio, television, has given each of us the opportunity to shape our ideas and find our audience. In other words, it has never been easier to go from consumer to producer of content. At the beginning of this revolution, we had the Internet. The Internet is the trigger for a worldwide democratization of access to and distribution of information. However, there is an industry that concerns us all which is also mainly based on information but which has not yet begun its transition to the Internet era: the financial industry.

The financial industry is one of the most heavily regulated industries with such high barriers to entry that it does not encourage new entrants or stimulate competition. However, there is an emerging movement that is on a mission to create new foundations for the financial industry by removing all the actual systemic constraints of traditional finance. This movement is called Decentralized Finance (DeFi) and it promises to bring the financial sectors, especially banking and insurance, into the Internet age where anyone would be able to create and distribute financial instruments, contracts and agreements today like you can create and distribute articles, videos, podcasts.

What are DeFi’s building blocks ?

First of all, as the Internet does not know how to manage value natively, Decentralized Finance is based on what is called the Internet of Value powered by the Blockchain technology.

Source: http://gatehub.net/blog/what-is-the-internet-of-value/

In short, the Internet of Value is a notion that has been built over the last ten years through three major innovations:

Bitcoin

First, Bitcoin, at its genesis, created the concept of digital scarcity, and thus alleviated one of the major problems of the Internet: giving a value to a piece of digital data. Bitcoin is also the first decentralized network and laid the foundation for DeFi. Indeed, thanks to its peer-to-peer protocol, Satoshi Nakamoto's Bitcoin network simply eliminated the intermediaries, the trusted third parties and allowed two people to send value directly to each other. Bitcoin introduced the first decentralized monetary system using Blockchain technology that is even being adopted by some countries like El Salvador as a legal tender.

Tokenization

Then, tokenization extends the concept of digital scarcity to any type of asset. It is the penetration of the Internet of Value into everyday life: Bitcoin is no longer viewed simply as the object of speculation by visionary technophiles, but as a technology with the potential to strongly affect the real world.

Smart Contracts

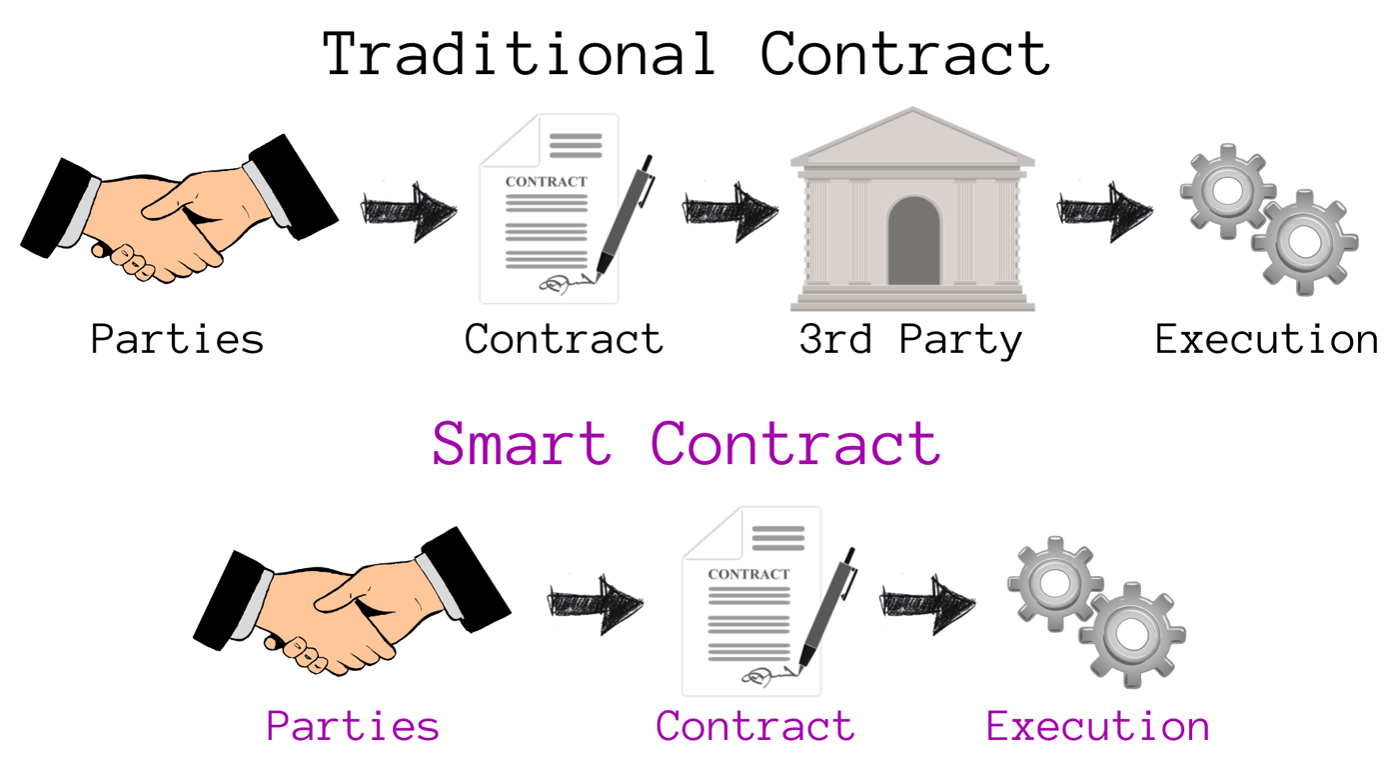

Finally, thanks to smart contracts, it becomes possible to program automatable or self-executing actions, thus opening the door to the creation of much more useful and complex financial services, all without a trusted third party, anywhere in the world.

Essentially, smart contracts are pieces of code that govern how certain applications function, all done autonomously. These applications are also known as dApps (for decentralized Applications). What keeps the legitimacy of smart contracts is that anyone can go in and verify or audit the code to ensure they are functional and fair and no one can tamper or change it after it is initiated. Smart contracts are like the engines of DeFi.

There are many platforms like Ethereum, Polkadot or Neo where you can already start using these decentralized financial products like loan platforms or exchanges.

It is with these fundamental building blocks at their disposal that, in recent years, entrepreneurs, engineers and organizations have begun to orchestrate not only new financial services, but quite simply a new global financial infrastructure, emancipated from traditional information systems, the preserve of historical and previously unavoidable intermediaries: this is the emergence of Decentralized Finance.

What is DeFi trying to do ?

DeFi is powering the next generation of financial instruments and services, a Blockchain-based ecosystem that allows anybody to access a variety of financial services without the need for a central authority. Bitcoiners have a saying: “Fix the money, fix the world”. But, what is the next step ? Fixing financial products. Mortgages, stock brokers, loans, insurance, bonds are all mediated by third parties who are frequently just as faulty as the money printers. DeFi is all about eliminating the points of failure that plague today's systems.

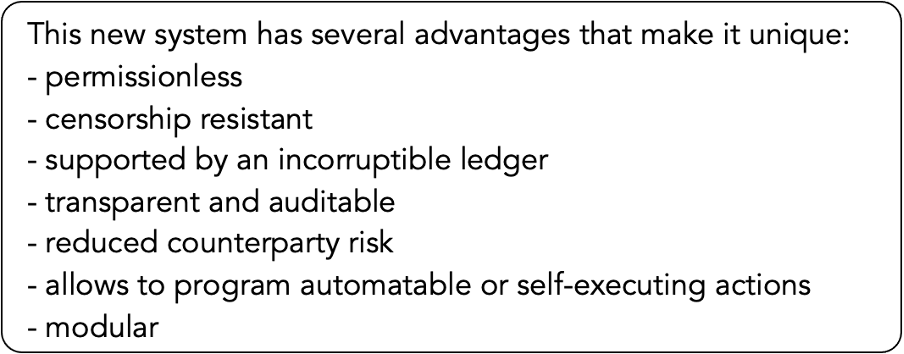

The two greatest strengths of this new system are that it is permissionless and censorship resistant. This means that any user could access loans, for example, without any discrimination. Today, access to technology is no longer the main barrier to accessing financial services. Indeed, most people outside the banking system have access to the Internet. Globally, of the 2 billion unbanked adults, two-thirds own a smartphone that can be used to access financial services. Most of the time, it is identity issues or political restrictions that prevent access to banks. Decentralized Finance wants to bring its services to everyone, at any time, without any restriction.

DeFi, in addition to removing all friction from overage fees, holding periods, and transaction restrictions, enables for the invention of new concepts and functions with money in ways that have never been possible before. It is for this reason that working with DeFi has been dubbed "money LEGOs".

Crypto Backed Stablecoins

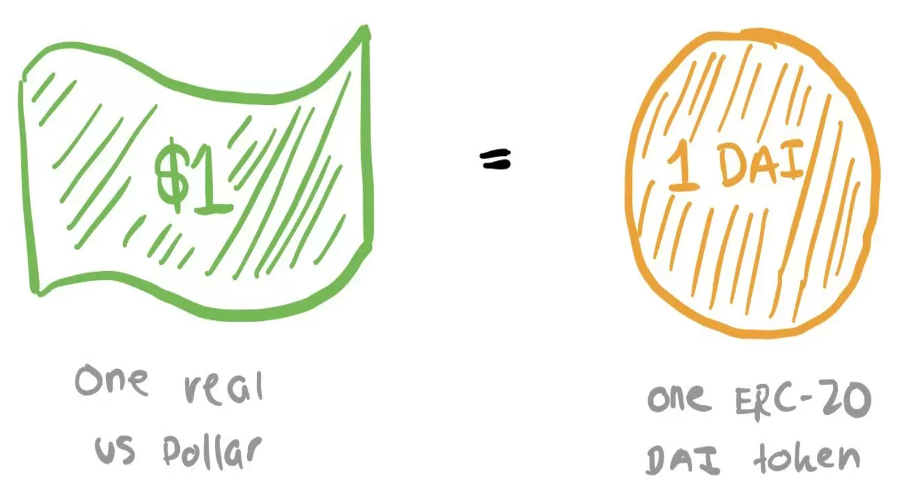

One of the most popular uses for cryptocurrency is stablecoins. Stablecoins are cryptocurrencies that hold their value on par with the US dollar. They are designed to minimize their volatility relative to an asset or basket of assets. Stablecoins protect you from the volatility of other crypto-currencies and serve as a reliable medium of exchange. It is therefore an essential component for making financial transactions. How do stablecoins work ? The first mechanism is quite simple: it consists of depositing $1 in a bank as a guarantee for each stablecoin. The stablecoins are backed by real dollars in reserves held by a third party. This mechanism requires you to place your trust in the intermediary who makes the deposit as well as in the bank that receives it. We cannot verify for ourselves that a stablecoin is always backed by $1. But, how do you create a stablecoin without a third-party reserve/intermediary ?

This is the second mechanism and it is more complex: it involves depositing cryptocurrencies such as Bitcoin or Ether in a smart contract as collateral for each stablecoin. Essentially, you back the value with another cryptocurrency. That is exactly what MakerDao does. MakerDao allows you to lock up your Ether as collateral to generate DAI which is another stablecoin that holds its value at $1 consistently. Each DAI is generated and backed by Ether that is locked up in smart contracts. For example, if 1 ETH = $2000, let us say you could generate $500 in DAI stablecoin by locking it up. If you want your Ether collateral back, simply pay back the loan by paying back the DAI. As long as ETH holds its value over $500, your collateral is safe as that DAI is fully backed by the collateral. And in the event that it does risk dropping under the value of the loan created, the collateral is automatically liquidated by the MakerDao smart contracts. With this mechanism, we do not need to trust an intermediary, but we do need to check that a stablecoin is always backed by an amount of cryptocurrencies with a higher market value.

What is the use for all of this ? It implies that cryptocurrency can be used to generate US dollars based loans or cash equivalents, allowing people to buy products and services without having to go to a bank or rely on their credit score. This also means that the value of your cryptocurrency can be used without having to sell it, which protects you from having to pay capital gains taxes on the sale of your asset.

Decentralized Exchanges

Exchange platforms are a must for financial transactions. It allows you to find a buyer or a seller for any type of assets: stocks, bonds, options, derivatives, etc... Traditionally, these platforms are custodians of the traded assets, meaning that if you want to use one of these platforms, you have to deposit your assets on it and therefore you lose control of them. As I mentioned earlier with stablecoins, this presents a risk of hacking or scamming since you are trusting an intermediary to manage your assets. This is where DEXs (Decentralized EXchanges) come in: this is our second component of decentralized finance. Unlike traditional platforms, decentralized exchange platforms use smart contracts to manage exchanges between cryptocurrencies. By doing so, no intermediary has control over your assets: we have solved the number one problem of centralized exchange platforms.

However, this is not the only problem, far from it. Another known problem is that of asset liquidity, i.e. the ability to buy or sell an asset quickly without major effects on its price. Traditionally, the liquidity of an asset on an exchange platform is represented by an order book. An order book allows you to see both the orders of those who wish to buy and those who wish to sell an asset with information such as the desired price and quantity. When there are few orders in the order book we end up with big price gaps between those who want to buy and those who want to sell the asset which leads to a situation where it is difficult or impossible to buy or sell an asset at the desired price and quantity. To solve this problem, exchange platforms use market makers who are paid intermediaries in charge of ensuring the liquidity of an asset by offering regular and continuous buying and selling prices for it. This allows for people to instantaneously buy and sell stocks, commodities or cryptocurrencies without instantaneously spiking or dropping the price.

In DeFi, it is a bit harder to do this as market makers in traditional finance often operate at around 1,000 to 1,800 transactions per second. Decentralized blockchains like Ethereum can only handle 10 to 30 transactions per second which on the surface makes it impossible to create and run a DeFi exchange that operates like a NASDAQ or a NYSE. To overcome this, decentralized exchanges like Uniswap or Pancakeswap have created things called liquidity pools. Essentially, these are pools of liquidity that replace market makers. Liquidity pools are mostly filled by what we call liquidity providers: users who provide liquidity for an asset for a fee. In some cases, these liquidity pools can pay out 100%+ per year in yield because there are a lot of fees generated based on the demand for the liquidity pool. In exchange for this considerably high interest, there is a risk of losing some of the funds to impermanent loss due to imbalance in the automated market making. If you own two sides to a market, for example ETH and DAI, you can put the ETH and the DAI together and lend them out into a pool. From there, Automated Market Makers (AMM), run by smart contracts, use algorithms to help buyers and sellers use liquidity within the pool, always making sure that there is a balance of the two assets within the market. The variation in the levels of the liquidity reserves between the two traded assets will allow the exchange to algorithmically set the price: the more an asset is bought, the more its price increases relative to the asset we are selling, conversely, the more an asset is sold, the more its price decreases relative to the asset we are buying. In short, we have an automated market maker that allows anyone to buy or sell an asset instantly.

Loan Platforms

Another application on DeFi is generating interest on your assets by lending it. For many of us, lending money is as simple as leaving it in our savings account. Lending platforms that make use of smart contracts like Compound or Aave expand our possibilities, this is our third component of DeFi. But unlike a savings account, an id or a credit score are not needed to take out a loan. You do not even need to sign up via email. All you need is the keys to your cryptocurrency wallet and trust on the smart contracts that govern the platform. These platforms also provide much better returns than savings accounts.

As with some decentralized exchange platforms, most decentralized finance lending platforms use liquidity pools. So on the one hand, there are lenders who fill the liquidity pool of an asset and collect interest, and on the other hand, there are borrowers who draw from the liquidity pool of an asset and pay interest on their debt. Interest is variable and algorithmically set according to the supply and demand for a certain asset. The more lenders that fill the liquidity pool of an asset, the more the interest reduces. Conversely, the more borrowers there are who draw from the liquidity pool of an asset, the more the interest increases. Thus, no time is wasted in searching for a counterparty and negotiating the terms of the loan. We can freely, without time constraint, lend, recover, borrow and repay an asset. However, there is an additional condition when you want to borrow an asset: you have to deposit as collateral an amount of cryptocurrencies with a higher market value than the borrowed assets, this is the same mechanism used by some stablecoins, which avoids the counterparty risk by ensuring the creditworthiness of borrowers. One advantage of decentralized lending platforms is that you do not need to collect your interest every year like with a savings account but continuously in real time with the ability to get your money and accrued interest back at any time.

Source: http://defi.cx/how-do-liquidity-pools-work/

Over the last year a lot of platforms like Compound have popped up which have sought to incentivize users to borrow or lend assets on their platform to improve things like liquidity for their ecosystem. Compound for instance paid users in a new governance token called COMP which it gave to users as a reward for borrowing or lending on the platform. As Compound grew with more users, more people wanted to own this governance token so they could have a say in the future of the platform thus leading to a huge demand for the COMP token and thus an increase in its price. So much in fact that the value of the COMP that was given out as a reward was often more than the interest cost to take out a loan or the interest generated by lending out assets. In layman’s terms, the reward of this COMP token was so great that you actually booked a profit for taking out a loan on Compound. And thus, spawned yield farming which is basically the act of going around to different decentralized finance platforms in search of the best yield and rewards. Since the COMP token emerged, many other platforms have created their own tokens to give away to their users as a form of reward.

DeFi in a few figures

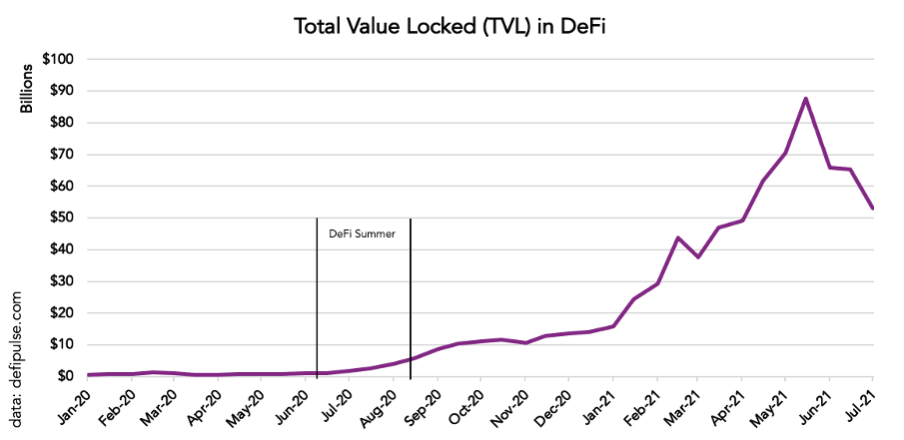

The market capitalization evaluation of DeFi is represented by the value of all the assets deposited by users within the protocols, also referred to as Total Value Locked, or TVL. This metric is the most widely used and fairest metric to assess the popularity of a DeFi protocol.

According to DeFi Pulse data, 1 year ago to the day, DeFi's TVL was only $2 billion. In just 12 months, the TVL of the DeFi ecosystem has consequently increased 25-fold, and now exceeds the $50 billion mark:

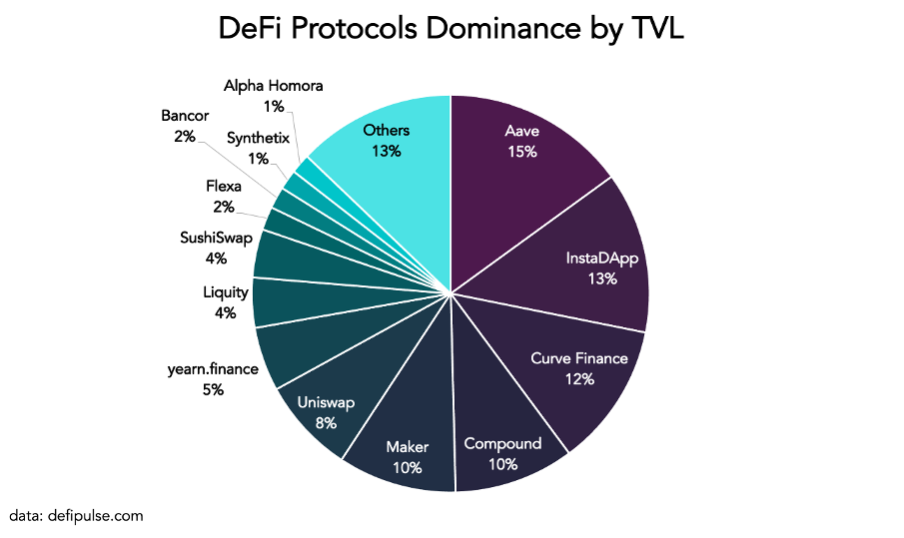

To date, the top 4 protocols in terms of TVL are Aave ($10.34 billion), InstaDApp ($9.07 billion), Curve Finance ($8.07 billion) and Compound ($6.73 billion). Between them, they account for half of the TVL, with Aave dominating by 15%:

We have seen 3 components of DeFi: stablecoins, decentralized exchange platforms, and lending platforms. These components can be combined without asking permission to create and distribute financial applications like we can fit LEGOs together to build constructions. Today, these financial applications are limited and reserved for a few insiders. It is as if we have gone back to the days of the first websites except that these applications operate on value and not information. So you have to be careful, because if the code is exploited or a flaw is discovered in an application that handles value, you can literally lose money. It is about making decentralized finance look like a construction made of LEGOs and not KAPLAs. There is still a lot of work ahead to make DeFi a secure place to put money into. But there is no doubt in my mind that these decentralized platforms will eventually compete with the centralized ones with the ethos of Bitcoin: transparency, immutability and full accessibility to anyone, anywhere.

Who could have imagined at the time of the first websites the infinity of applications we have today to create and distribute content? No one and I am convinced that we are at the very beginning of a wave of financial applications that will democratize value on the internet in the same way that the applications we use today have democratized information on the internet. The Google and Facebook of tomorrow will be those who understand and seize this opportunity.